In today’s increasingly urgent climate context, Environmental, Social, and Governance (ESG) performance is no longer a “nice-to-have” soft capability—it has become a hard metric critical to a company’s long-term survival and market competitiveness. While many executives recognize the importance of low-carbon transition, they often struggle in practice: How can the grand “carbon neutrality” goal be translated into concrete actions across departments and business units? How can carbon management evolve from a cost center into a core driver of value creation?

Perhaps the answer lies in an innovative management tool: Internal Carbon Pricing (ICP).

What Is Internal Carbon Pricing?

As of 2023, 1,722 companies globally reported to CDP that they have already implemented internal carbon pricing mechanisms, and another 3,070 companies indicated plans to adopt such mechanisms within two years.

Source: CDP, Abatable 2025

In traditional corporate operations, carbon emissions are typically treated as an externalized environmental cost that is difficult to quantify. Internal carbon pricing, however, is an innovative financial strategy that assigns a clear monetary value (e.g., price per ton of CO₂ equivalent) to a company’s own emissions. The brilliance of this mechanism lies in its ability to convert uncertain future risks—such as carbon regulation or carbon taxes—into quantifiable and manageable economic costs today, thereby “internalizing” external environmental costs and putting a clear price tag on emissions.

At its core, internal carbon pricing is an advanced financial and management tool that breaks down traditional departmental decision-making silos and reshapes the entire logic chain—from strategy to operations—providing a governance framework for low-carbon transformation that is flexible, incentive-driven, and executable.

Main Forms of Internal Carbon Pricing

There is no one-size-fits-all approach to implementing internal carbon pricing. Currently, five primary forms are widely used: implicit pricing, shadow pricing, emission offsets, internal carbon fees, and internal emissions trading. These vary significantly in complexity and operational impact.

Main Forms of Internal Carbon Pricing

Among these, shadow pricing—a hypothetical price—is the most widely applied, primarily used by senior leadership for strategic investment risk assessment and decision optimization without involving actual cash flows. Implicit pricing, derived from historical abatement costs, provides an internal benchmark for project evaluation. When companies seek tangible financial incentives and behavioral change, they may adopt an internal carbon fee, charging departments and establishing a dedicated fund to drive emission reductions. Internal emissions trading is more complex, using allocated quotas and internal trading to achieve cost-optimal reductions through market mechanisms. In contrast, emission offsets focus on leveraging external markets to fulfill reduction commitments, offering flexibility in meeting targets.

Companies can flexibly select or combine approaches based on their specific goals, organizational structure, and decarbonization progress.

How Does Internal Carbon Pricing Drive Corporate Low-Carbon Transition?

Internal carbon pricing is not an isolated financial tool but a powerful decision-making engine. Specifically, it drives low-carbon transformation through five interconnected dimensions:

1. Strategic Decision-Making: Accelerating the Shift Toward Low-Carbon Operations

Under traditional business inertia, companies struggle to adjust short-term behavior based on long-term climate risks. As a systematic evaluation tool, internal carbon pricing quantifies sustainability risks by simulating medium- to long-term carbon regulations and costs, embedding them into core strategic decisions and strongly steering investments and business portfolios toward low-carbon areas.

2. Operational Management: Reducing Cross-Departmental Collaboration Costs for Emission Reduction

Decarbonization efforts often face challenges in cross-departmental communication and resource coordination. Internal carbon pricing establishes an internal carbon market or carbon fee fund, providing systematic financial support for reduction projects and reducing inter-departmental competition for resources. By quantifying emissions as a cost, it incentivizes departments to proactively optimize technologies and strengthen supply chain management, fostering an operational mindset where “emission reduction equals cost saving.”

3. Financial Planning: Transparent Carbon Costs Enable Optimal Resource Allocation

In traditional financial models, carbon costs are often seen as unquantifiable external risks. Internal carbon pricing internalizes them as explicit economic costs, allowing companies to precisely incorporate carbon factors into budgeting and investment decisions, enhancing the foresight and accuracy of financial planning. For example, revenues from internal carbon trading can be earmarked for low-carbon technology investments, creating a virtuous closed-loop funding cycle.

4. Innovation Incentives: Driving Green Technology Innovation, Sharing, and Implementation

Under traditional KPI-driven departmental reduction models, departments often lack motivation for over-performance. With internal carbon pricing, any cost savings from emission-reducing innovations—whether technological or managerial—directly translate into departmental economic benefits. This transforms emission reduction from a “cost burden” into a potential “value source.” This fundamental shift in incentives provides sustained internal momentum for green innovation and encourages the proactive discovery, sharing, and scaling of best practices.

5. Risk Management: Proactively Identifying Potential Carbon-Related Risks

A core function of internal carbon pricing is to serve as a “stress test.” By simulating future carbon prices or policy-driven carbon costs, it helps companies proactively identify and flag potential financial risks, prompting management to plan low-carbon transition pathways in advance, effectively hedging against policy volatility and enhancing operational resilience and sustainability.

Case Study – Mitsubishi Materials

To accelerate its 2045 carbon neutrality goal, Mitsubishi Materials Corporation implemented an internal carbon pricing system in April 2024, setting the price at a high level of 10,000 JPY per ton of CO₂.

The system specifically targets capital investment decisions that directly reduce the company’s own operational emissions (Scope 1 and 2). By converting emission reductions into significant virtual cost savings, it aims to strongly promote the adoption of energy efficiency improvements and clean energy technologies, enabling deep decarbonization in a more cost-effective manner.

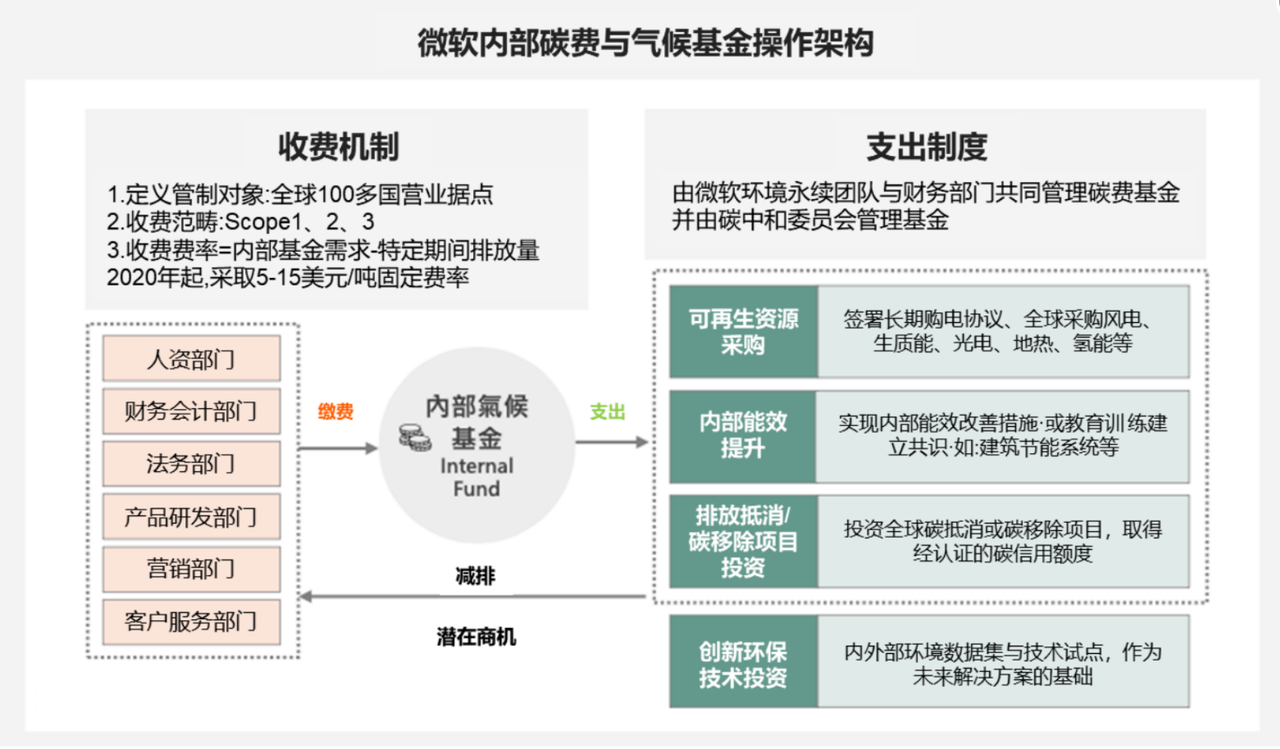

Case Study – Microsoft

Microsoft uses fees based on Scope 1, 2, and 3 emissions to fund renewable energy, offsets, technological innovation, and internal emission reduction and energy efficiency projects. Business Units (BUs) can track their emissions and associated fees in real time throughout the year. Management regularly discusses the application of internal carbon pricing with finance and BU leaders to ensure implementation considers each BU’s specific context while aligning with the overall corporate strategy.

Source: www.microsoft.com

How Can Internal Carbon Pricing Enhance

a Company’s ESG Management Practices and Ratings?

In ESG rating frameworks, a company’s capacity and effectiveness in managing climate-related issues have become core criteria for assessing sustainability performance. Leading ESG rating agencies—including MSCI, Sustainalytics, CDP, and FTSE Russell—all consider a company’s climate risk response strategies, ability to implement emission reduction targets, and use of carbon management tools as key indicators of ESG performance. The establishment and application of an internal carbon pricing mechanism directly aligns with these requirements, clearly signaling to rating agencies and investors the company’s systematic planning and proactive stance on climate governance—making it a critical enabler for ESG rating improvement.

From the perspective of rating logic, internal carbon pricing not only demonstrates a company’s financial acumen in internalizing external climate costs but also showcases its governance capability to integrate carbon management into core business strategy. This practice of “transforming climate risk into management opportunity” embodies the core sustainable development philosophy advocated by rating agencies, effectively strengthening a company’s competitiveness in ESG assessments and providing investors with quantifiable, trustworthy signals of climate governance—ultimately helping the company gain recognition and favor in capital markets.

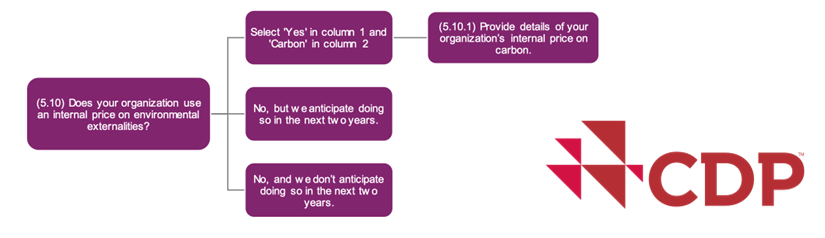

CDP Rating Requirements on Internal Carbon Pricing

To achieve a high CDP score, companies must establish an internal carbon pricing system and disclose detailed information about it, enabling investors to assess the quality of the methodology and understand how and why internal carbon pricing is used to evaluate and manage carbon-related risks and opportunities in operations, supply chains, and investments.

Source: CDP Full Corporate Scoring Methodology 2025 – Climate Change

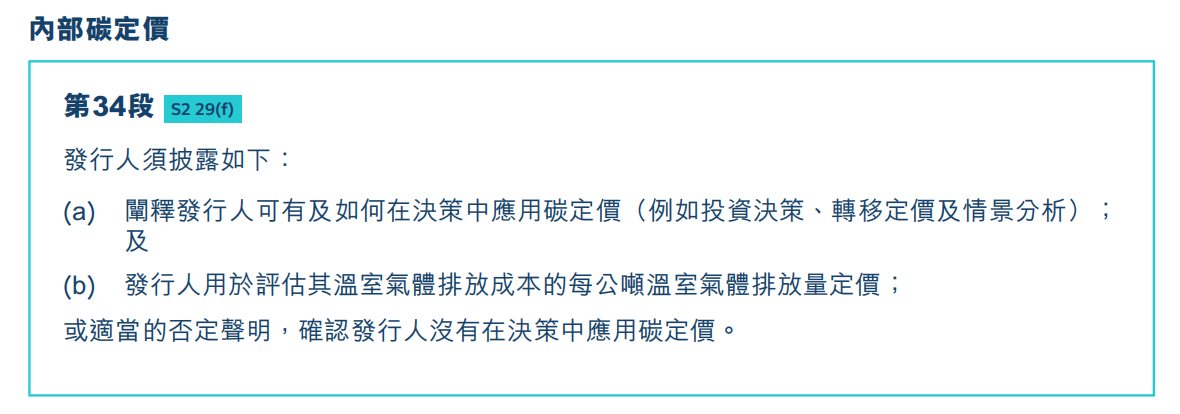

Hong Kong Exchanges and Clearing (HKEX) Encourages Issuers to Use Internal Carbon Pricing for Quantified Decision-Making

HKEX explicitly supports internal carbon pricing but adopts a “comply or explain” disclosure principle. Its core requirement is that issuers must disclose in their ESG reports whether and how they apply internal carbon pricing (including the price level) in decision-making; if not applied, a negative statement is required. While not mandating all issuers to implement such a mechanism, HKEX actively encourages adoption, noting that it effectively helps quantify the financial impact of carbon footprints and optimize decisions. It also expects concerns about disclosing commercially sensitive information to diminish as carbon markets mature.

Source: “HKEX Guidance on Implementing Enhanced Climate Disclosures under the Optimized ESG Framework”

GRI Recommends Disclosure of Internal Carbon Pricing Mechanism Development

Under GRI 102, organizations should systematically describe their governance structure when reporting climate transition plans, including disclosures on incentive mechanisms linking transition target performance to compensation of board members and senior executives. Additionally, GRI recommends that companies report whether they have established an internal carbon pricing mechanism and specify its coverage, price level, and methodology to comprehensively demonstrate how strategic governance and management tools are used to address climate-related risks and drive the transition to a low-carbon economy.

1. Environmental Dimension: Quantified Management as “Hard Evidence” of Ambition

- Improves “Climate Risk Management” scores: Internal carbon pricing demonstrates a systematic, forward-looking climate risk management framework rather than passive reaction.

- Strengthens “Emissions Targets and Performance”: Internal carbon pricing is a key enabler for ambitious goals like Science-Based Targets (SBTi). Rating agencies see not just targets, but credible implementation tools.

- Enhances “Resource Use and Circular Economy” metrics: Energy efficiency and process optimization driven by internal carbon pricing directly reduce resource consumption, improving related performance data.

2. Governance Dimension: Top-Level Design Reflects “Excellence in Governance”

- Demonstrates “Board Oversight and Risk Management”: Implementing internal carbon pricing typically requires board or top-management approval, directly reflecting the company’s commitment to integrating climate change into core governance.

- Shows “Incentive Alignment with Long-Term Strategy”: Linking carbon costs to performance evaluations indicates that executive compensation is tied to long-term sustainability goals—a hallmark of high-quality corporate governance.

3. Social Dimension: Indirect Empowerment Builds a Responsible Brand Image

- Attracts and retains talent: Especially among younger generations, who prefer working for socially and environmentally responsible companies. Leading low-carbon practices serve as a powerful “employer brand.”

- Builds trust with customers and communities: A proactive stance on climate action significantly enhances brand reputation and customer loyalty.

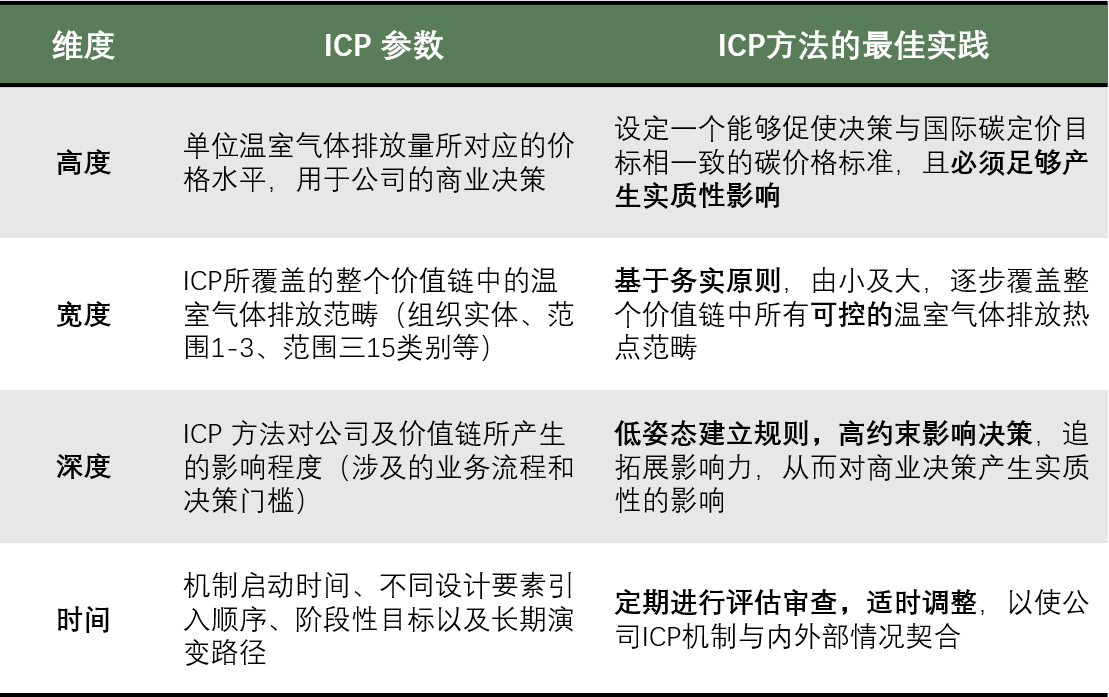

Key Dimensions for Designing and Implementing

an Internal Carbon Pricing Mechanism

To achieve optimal results, companies should design and implement internal carbon pricing mechanisms along four key dimensions: price level (“height”), scope of greenhouse gas emissions covered (“width”), degree of impact on business operations (“depth”), and timing aligned with the decarbonization roadmap (“time”). Companies can dynamically set and adjust their mechanisms based on internal and external contexts.

Four Dimensions of Internal Carbon Pricing Mechanism Design

Carbonstop Helps Enterprises Build

Scientific and Actionable Internal Carbon Pricing Mechanisms

As a pioneer in advanced carbon management, Carbonstop employs a unique “consulting-led, software-enabled” model to help clients establish scientific and actionable internal carbon pricing mechanisms that support low-carbon transition and ESG goals. Our consulting team handles top-level design and mechanism development to ensure scientific rigor and alignment with business realities. Meanwhile, our AI and software development teams leverage the Carbon Cloud SaaS platform to digitize and automate the mechanism—enabling integrated management of data collection, quota allocation, price setting, cost accounting, and performance tracking—ultimately forming a sustainable “manage-execute-feedback” optimization loop to empower efficient carbon management.

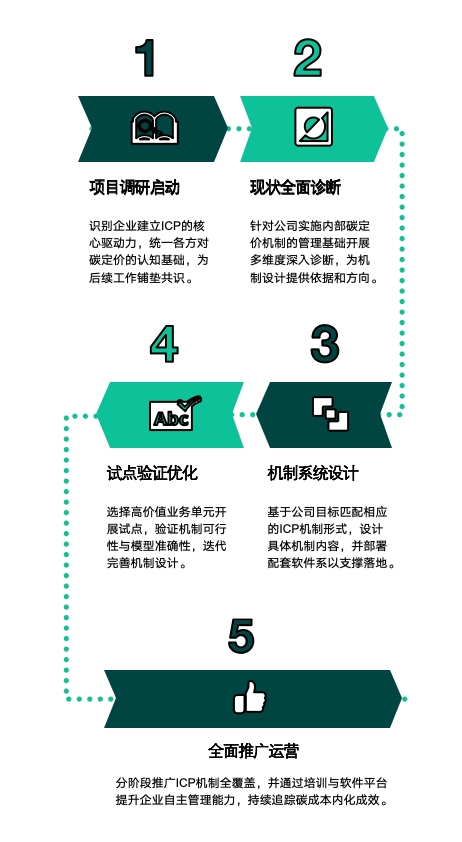

Specifically, we follow a five-step approach to ensure steady progress in your internal carbon pricing implementation:

Carbonstop’s Service Pathway for Internal Carbon Pricing Mechanism Development

Implementing internal carbon pricing is a strategic transformation. Its success hinges on deep understanding of business strategy and precise navigation of organizational change—not merely technical execution. Carbonstop’s value lies in being your strategic partner, not just a solution vendor.

- Strategic Insight and Forward-Looking Planning: We deeply understand the intersection of ESG rules, capital market expectations, and real-world operations, ensuring your internal carbon pricing mechanism not only meets compliance needs but also directly serves your core business objectives.

- Cross-Industry Best Practice Enablement: We bring proven insights from diverse sectors to help you avoid common pitfalls and prioritize high-value scenarios that deliver “high impact with modest investment.”

- Highly Customized and Confidential: We recognize each company’s uniqueness and the sensitivity of proprietary methodologies. Our collaboration is tailored to your specific goals, ensuring high relevance and strict confidentiality to jointly protect your competitive advantage.

Contact us to schedule an exclusive Internal Carbon Pricing Implementation Strategy Workshop for your organization, and explore with our expert advisors the specific applications and potential value of internal carbon pricing in your enterprise.