The EU Carbon Border Adjustment Mechanism (CBAM) is no longer a distant regulatory prospect. As we enter 2026, the transition from administrative reporting to financial obligation marks a structural shift in international commerce. For global exporters, CBAM is not merely an environmental tax. It represents a fundamental change in how companies access markets, and this means that the quality and credibility of verified carbon data is becoming as critical as product quality.

CBAM ensures that the carbon costs of imported goods in sectors such as cement, iron and steel, aluminum, fertilizer, electricity, and hydrogen mirror the costs borne by EU producers under the Emissions Trading System (ETS). By linking imports directly to their embodied carbon, the CBAM EU framework effectively extends climate pricing beyond European borders, ensuring a level playing field. This is reducing the risk of carbon leakage and neutralising the competitive advantage of overseas producers in jurisdictions where climate regulation is weaker.

The Definitive Phase: From Reporting to Financial Liability

The Definitive Phase: From Reporting to Financial Liability

In 2026, the stakes for affected sectors and companies will increase materially. While the transitional phase (which began in October 2023) focused on emissions reporting and data collection, the definitive phase introduces the requirement to purchase and surrender CBAM certificates. The cost of these certificates is linked directly to EU ETS prices, although the regulation allows for a critical adjustment: a deduction for any carbon price already paid in the country of origin.

For companies within the affected sectors, the financial implications are clear.

Companies that can provide verified, actual emissions data (the precise carbon footprint of their specific product or facility) can prove they are less carbon-intensive than the EU's default assumptions, which directly reduces the number of CBAM certificates they must purchase.

Conversely, exporters who are unable to provide this verified data are subject to the use of 'default values'. These values are effectively a high-level safety estimate set by the EU. They are intentionally conservative and punitive, typically based on the average emissions intensity of the dirtiest or 'worst-performing 10%' of EU installations for that product type.

Relying on these elevated default values means paying a significantly higher carbon tax than your product might actually warrant—often resulting in a 30-50% higher financial penalty than your true footprint. For exporters, this is a direct and substantial hit to the bottom line.

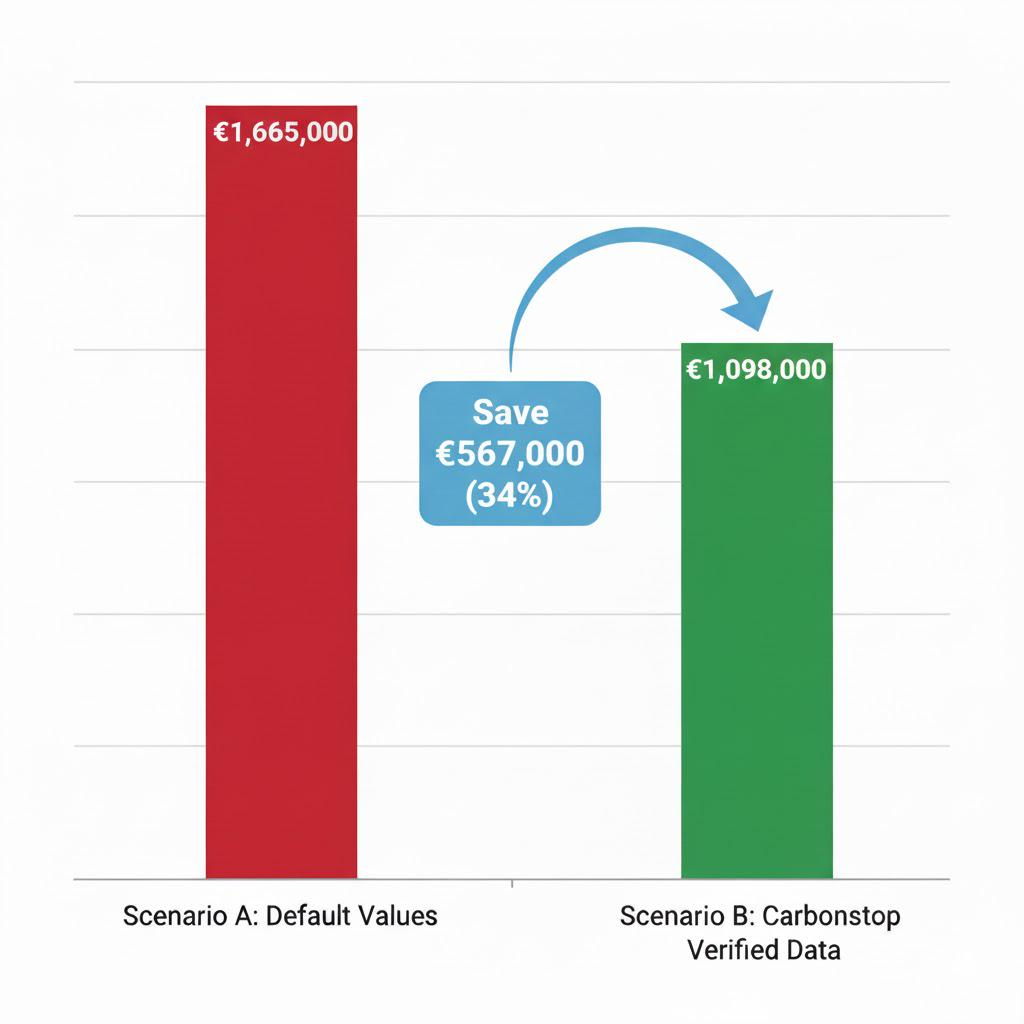

To illustrate the financial impact of data transparency under CBAM 2026, a comparative model for an exporter of 1,000 tonnes of primary aluminium shows that using default values under CBAM 2026 can result in substantially higher financial liability than using verified actual emissions data managed through a digital carbon management system such as Carbonstop.

Table: Example importing 1000 tonnes of aluminiu

| Scenario A: EU Default Values | Scenario B: Carbonstop Verified Data | Potential Savings | |

| Emissions | 18.5 tCO2e | 12.2 tCO2e | -34% Intensity |

| CBAM Certificates Required | 18,500 | 12,200 | 6,300 |

| Total Carbon Cost (estimated at €90/tCO2e) | €1,665,000 | €1,098,000 | €567,000 |

*Estimated costs are based on the EU Carbon Border Adjustment Mechanism projected carbon price of €90/tCO2e

Strategic Implications for Green Transition

Strategic Implications for Green Transition

The impact of CBAM is particularly relevant for key manufacturing sectors that are driving the green transition, such as electric and hybrid vehicles, lithium-ion batteries, and photovoltaic (PV) products. While these categories are central to global decarbonization efforts, they rely heavily on CBAM-covered materials (like iron and aluminum). Consequently, their lifecycle carbon footprints are now under intense scrutiny from EU regulators, especially under complementary laws like the New Battery Regulation and the CSRD.

As a result, exporters are increasingly encouraged to move beyond using average or proxy emission factors. Maintaining market access and competitiveness will depend on the ability to demonstrate product- and facility-specific carbon performance. As a result, sustainability is no longer a discretionary; it is a needed for continued access to EU markets.

Operationalising Compliance: The Data Integrity Gap

Operationalising Compliance: The Data Integrity Gap

The core operational challenge for CBAM 2026 is the accurate assessment of embedded emissions (the carbon footprint of the imported goods). This calculation must precisely account for both Scope 1 and Scope 2 emissions, with the results mapped rigorously to the relevant CN (Customs Nomenclature) codes for EU declaration.

Success in meeting these audit-ready requirements rests on three critical operational pillars:

1.Supply Chain Traceability: Moving Beyond Spreadsheets

Collecting verifiable, primary data from upstream suppliers is difficult given today's fragmented global value chains. Manual processes and spreadsheets are no longer sufficient to support the audit-ready transparency demanded by the EU.

2.Localised Accuracy

Global average emission factors often fail to reflect the operational realities of specific manufacturing hubs. The use of China-specific emission factors, where relevant, allows exporters to move away from conservative international defaults and more accurately reflect their actual carbon intensity—often resulting in lower CBAM exposure.

3.Third-Party Verification

All emissions data must be formally verified by an EU-accredited body. Preparing the necessary verifiable documentation is therefore an ongoing operational requirement, integrated into workflow, rather than a quarterly or annual reporting exercise.

The Carbonstop Advantage: Turning Regulation into Resilience

Navigating CBAM at scale requires enterprise-grade carbon management infrastructure. Carbonstop provides the technical foundation to bridge the gap between production data and regulatory compliance.

Carbonstop provides the technical foundation to manage this complexity. Our platform applies AI-driven validation to pre-audit supplier and facility-level data, identifying anomalies, data gaps, and any inconsistencies. This process ensures the data is of high quality, allowing exporters to prepare defensible, audit-ready CBAM EU reports. Furthermore, by leveraging our extensive and regionally granular emissions factor database, clients can use verified data that accurately reflects their actual, lower-carbon production performance.

Carbonstop also aligns carbon accounting processes with international frameworks including the GHG Protocol, CSRD, and ISSB, ensuring that a single source of truth supports both CBAM compliance and broader corporate reporting obligations.

Looking Ahead: A Harmonised Global Market

Looking Ahead: A Harmonised Global Market

CBAM is widely viewed as the first of several carbon-aligned trade measures. Similar approaches are under consideration in jurisdictions including the UK, Canada, and Japan. The direction of travel toward carbon-adjusted trade is clear.

Exporters that act early to digitise emissions accounting and engage their supply chains will be better positioned to manage regulatory risk and differentiate themselves in increasingly carbon-sensitive markets.

Is your supply chain ready for the 2026 financial surrender?

Is your supply chain ready for the 2026 financial surrender?

Contact Carbonstop for a CBAM Financial Impact Assessment and understand how an AI-enabled, audit-ready carbon management platform can help reduce regulatory exposure.

FAQ

Q1: How can exporters deduct carbon prices already paid outside the EU Carbon Border Adjustment Mechanism rules?

Under CBAM Article 9, importers may claim a reduction in the number of CBAM certificates surrendered based on the carbon price effectively paid in the country of origin (for example, under China’s national ETS). This requires verified documentation demonstrating that the price was legally mandated, paid, and not subject to export rebates. Carbonstop’s audit-ready reports include structured fields for carbon price documentation to support this process.

Q2: What are the “default values” for 2026, and why are they high?

If actual emissions data is unavailable or unverified, default values are applied. These are typically based on conservative benchmarks reflecting high-emission installations in the EU. The intention is to incentivise transparency and accurate reporting. For many exporters, reliance on default values can materially increase CBAM costs relative to actual emissions performance.

Q3: Does CBAM 2026 require Scope 3 emissions reporting?

The focus of CBAM is on embedded emissions, covering Scope 1 and Scope 2 emissions from production. While it does not require full Scope 3 reporting, it does require emissions data for certain upstream precursors. Carbonstop’s supplier engagement tools are designed to support this requirement.

Q4: How does the phase-out of EU ETS free allocations affect CBAM 2026 certificate pricing?

CBAM is designed to replace the free allocation of EU ETS allowances. Between 2026 and 2034, free allocations will gradually decline. During this period, CBAM charges apply only to the share of emissions not covered by free allowances, meaning CBAM costs will increase progressively over time.

Q5: Can AI-supported validation replace third-party verification?

No. Verification must be performed by an EU-accredited verifier. However, AI-supported validation can act as a pre-audit layer, identifying potential issues before formal verification. This can significantly reduce audit effort and the risk of non-compliance.