The SBTi Corporate Net-Zero Standard has become the most influential framework for turning corporate climate ambition into science-based action. For CSOs and sustainability leaders, it does more than set targets. It shapes how net-zero commitments get defined, validated, reported, and governed across Scope 1, 2, and 3 emissions.

The latest developments deserve close attention. The SBTi Corporate Net-Zero Standard Version 2.0 is currently a draft. It is not a final adopted standard. Read it as a strong directional signal, not a rulebook. But don’t dismiss it either. The draft points toward a more rigorous, more cyclical and substantially more data-intensive model for net-zero target-setting.

The upshot for businesses: the hard part is no longer making the commitment. It’s building the data quality, supplier engagement programmes, transition plans, and reporting discipline to back it up.

What the SBTi Net Zero Standard Is Designed to Do

What the SBTi Net Zero Standard Is Designed to Do

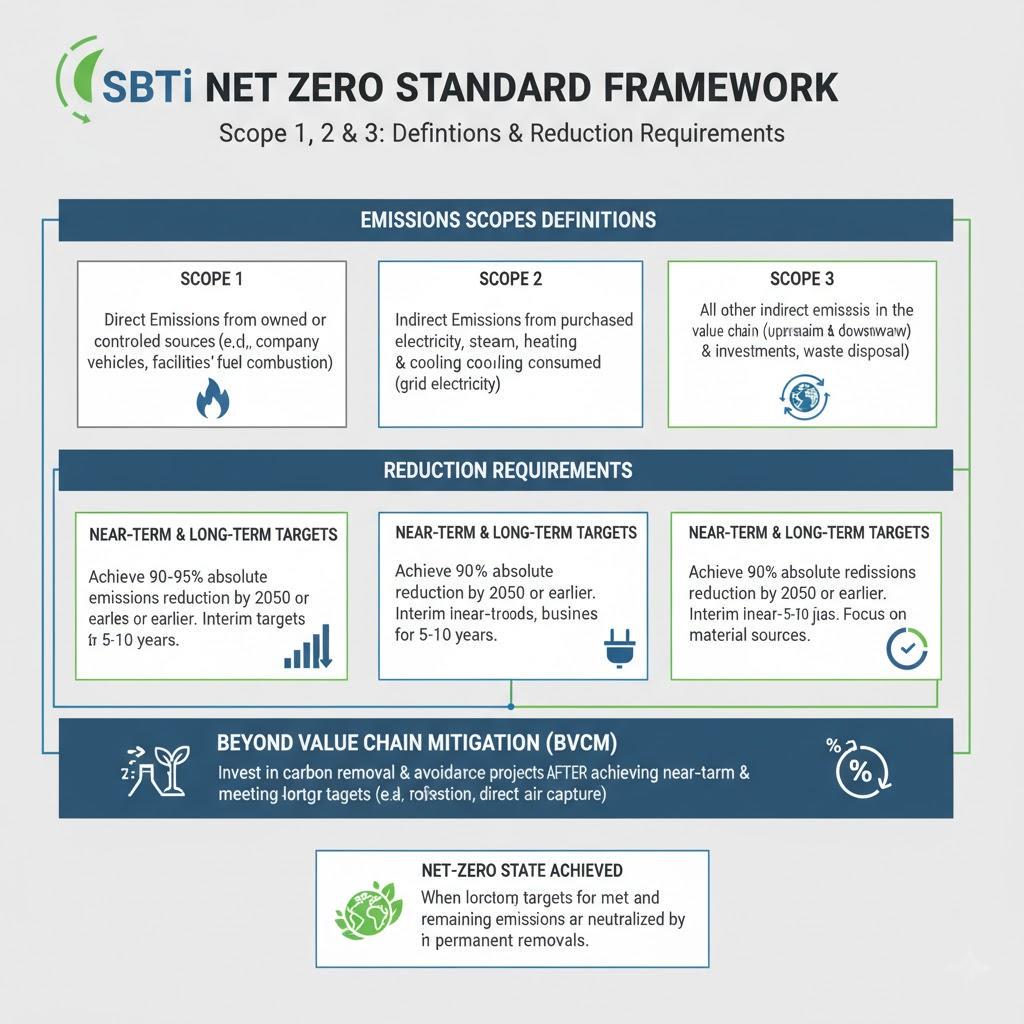

The standard gives companies a framework for aligning emissions reduction targets with climate science and the goal of limiting warming to 1.5°C. It requires deep reductions across the value chain—not offsets as a substitute for decarbonisation. The framework covers Scope 1 (owned or controlled sources), Scope 2 (purchased energy) and Scope 3 (the full value chain).

None of that is new. What’s changing is how specific the standard is becoming about validation mechanics, ongoing obligations, material Scope 3 categories and evidence of progress over time.

What Is Changing in the Draft Standard and Why It Matters

The draft marks a real shift: from a one-time target validation event toward continuous performance management and governance. Five changes stand out.

Cyclical Validation and Ongoing Oversight

Perhaps the most consequential proposal is cyclical validation. The draft replaces the current one-and-done model with a sequence: Entry Check, Initial Validation, Renewal Validation, and Spot Checks. Companies won’t be able to secure approval and move on. They’ll need to keep their emissions data, methodology notes, and governance processes audit-ready on a rolling basis.

That’s a different kind of operational demand. Teams accustomed to pulling data together once every few years for a validation cycle will need version-controlled reporting workflows and structured data trails that hold up to external scrutiny at any point. Without them, renewal and spot checks become genuinely difficult.

Company Categorisation and Differentiated Requirements

The draft introduces Category A and Category B companies. The distinction is broadly based on company type and scale, and it determines which requirements apply and how much flexibility a company gets. Category A (larger or higher-impact organisations) faces the most demanding expectations, including that 12-month transition plan deadline.

If this provision survives into the final standard, many Category A companies will face a tight implementation window. Especially those that haven’t yet built the governance infrastructure to support a credible transition plan on that timeline. The differentiated model makes sense in principle, but it puts a premium on understanding quickly where your company falls and what follows from that classification.

Stronger SBTi Transition Plan Requirements

The draft pushes harder on transition planning. Category A companies would need to publish a transition plan within 12 months of Initial Validation. That’s a tight window and it shifts the conversation from “do you have a target?” to “can you explain, with specifics, how you’ll hit it?”

As renewal and spot-check cycles bring them under third-party review, the quality of what’s behind them matters including data provenance records, emission factor sourcing documentation, methodology notes, change logs. Auditability and transparency become prerequisites, not aspirational qualities.

A More Focused Approach to Scope 3 Target Setting

Scope 3 is still central, but the draft takes a more targeted approach focusing on significant categories and priority emissions sources rather than requiring blanket coverage across all fifteen categories. On paper, that’s more practical. But it also forces companies to justify which categories they’ve prioritised and show that the data underneath is getting better over time.

Here’s where it gets difficult for companies with complex global supply chains. When manufacturing, raw materials, or logistics are concentrated in regions like China, the generic emission factor databases most companies rely on, built primarily on European and North American data, don’t accurately reflect local grid intensity, process-level energy consumption, or regional fuel mixes. The gap between what those databases assume and what’s actually happening on the ground grows more consequential as the standard demands higher-quality, category-level Scope 3 accounting. Closing it requires localised datasets and supplier engagement programmes that can capture primary data at scale.

Ongoing Emissions Responsibility and Neutralisation

The draft draws sharper lines between three distinct concepts: emissions reductions, responsibility for ongoing emissions, and neutralisation of residual emissions at the net-zero target year and beyond. This matters because market commentary tends to collapse these into a simple “offsets versus reductions” debate, which misses the point. Corporate leaders will need to understand and report on the different mechanisms for addressing residual emissions, and demonstrate that any investment in carbon credits or removals complements deep decarbonisation rather than substituting for it.

How to Prepare for SBTi Net Zero Standard 2.0

The draft is clear enough about direction that waiting for the final text is a losing strategy. The companies that move now will be better positioned regardless of where specific provisions land.

Stress-test your current target architecture. If you already hold validated science-based targets, ask a blunt question: would your data, governance, and reporting hold up under cyclical review? Could you produce audit-ready documentation at short notice for a spot check? If the honest answer is no, that’s the first priority.

Get serious about Scope 3 data quality. Identify which categories are genuinely material. Improve supplier coverage. Reduce reliance on generic emission factor averages where better data is available or obtainable. For supply chains running through Chinese manufacturing or procurement, assess whether your current datasets reflect local conditions or are built on assumptions the draft standard may no longer tolerate.

Build a transition plan that can survive scrutiny. If your company has a net-zero commitment, make sure there’s a credible implementation pathway behind it. The pathway should connect decarbonisation levers, capex allocation, supplier engagement, and operational changes in enough detail to withstand external review.

Treat carbon data as infrastructure. The companies that adapt fastest to evolving standards are those with strong internal controls, scalable data systems, and workflows built for audit and not for one-off reporting exercises. This aligns with the broader direction of CSRD, ISSB, and investor-grade disclosure requirements. The organisations that get data infrastructure right will find everything else from target validation, transition planning, Scope 3 reporting materially easier.

How Carbonstop Supports SBTi Readiness

Cyclical validation, Scope 3 data quality in complex supply chains, transition plan credibility, audit-ready reporting—these are the challenges the draft standard is sharpening, and they’re the problems Carbonstop’s platform was built to solve. Carbonstop provides enterprise carbon data management across Scope 1, 2, and 3, with supplier engagement workflows designed to improve value-chain data collection at scale. Its AI-powered validation catches anomalies, gaps, and inconsistencies in emissions data before they surface during external review.

For companies wrestling with the Scope 3 data gap in global supply chains, particularly those with manufacturing or procurement exposure in China, Carbonstop offers localised emission factor datasets reflecting regional grid intensity, industrial process profiles, and fuel mixes. That means less dependence on generic assumptions and stronger, more defensible category-level Scope 3 accounting. It’s a direct response to one of the toughest requirements the final standard is likely to carry forward.

The Strategic Takeaway

Don’t treat the draft SBTi Net Zero Standard 2.0 as a finalised rulebook. Treat it as a clear signal of where corporate climate governance is going: tighter validation cycles, continuous oversight, stronger Scope 3 expectations, and an explicit demand that targets come with credible plans for delivery.

Net zero is becoming less about the commitment and more about the execution. The organisations that build the right data foundations, supplier engagement capabilities and reporting infrastructure now are the ones that won’t be scrambling when it does.

Assess Your SBTi Readiness

Is your organisation prepared for where the SBTi Net Zero Standard is heading? Carbonstop offers a Scope 3 Readiness Diagnostic for companies reviewing their science-based targets against emerging validation, Scope 3, and transition planning requirements.

Request your diagnostic to evaluate your Scope 3 data quality, reporting workflows, and transition plan readiness against the draft SBTi Corporate Net-Zero Standard 2.0.