On April 7, 2026, the European Commission announced the CBAM certificate price for the first quarter of 2026: EUR 75.36 per tonne. This is the first certificate price with real practical significance since CBAM formally entered its levy phase, signaling that the mechanism is moving beyond policy discussion and data reporting into a real cost factor that companies must carefully assess and prepare for.

What Is CBAM, and Why Does It Matter More Now?

CBAM, short for the Carbon Border Adjustment Mechanism, is commonly referred to as the EU Carbon Border Adjustment Mechanism and is often informally understood as a kind of “EU carbon tariff.”

Its core logic is that the EU wants imported products to bear carbon costs comparable to those faced by domestic producers, thereby avoiding so-called “carbon leakage,” where high-emission products gain a cost advantage through imports due to differences in carbon pricing across countries and regions.

In terms of scope, CBAM currently focuses on carbon-intensive sectors such as iron and steel, aluminum, cement, fertilizers, electricity, and hydrogen, along with certain precursor products. It may expand in 2028 to cover around 180 downstream steel- and aluminum-intensive products, with potentially significant implications for industries such as machinery and equipment, automotive and auto parts, household appliances, hardware, and metal products. For Chinese companies, any business tied to the EU market means CBAM is no longer just something to monitor from a policy perspective—it is becoming a real requirement in customer questionnaires, supply chain disclosure, product accounting, and compliance preparation.

More importantly, CBAM has already entered a new implementation stage:

• On January 1, 2026, the formal phase of CBAM began;

• On April 7, 2026, the European Commission published the Q1 2026 CBAM certificate price, providing the market with its first official pricing reference.

In other words, the question companies face is no longer whether CBAM will arrive, but how much impact it will have once it does.

How was the price of EUR 75.36 per tonne determined?

The announced price of EUR 75.36 per tonne is not a fixed administrative price set arbitrarily. Rather, it is the result of a calculation carried out under the EU’s established mechanism.

According to the European Commission’s public explanation, CBAM certificate prices in 2026 will be published quarterly, with one price per quarter. The price is determined based on the weighted average of the EU ETS auction clearing prices for the relevant quarter. In other words, the CBAM certificate price is directly linked to the EU carbon market, with the aim of aligning the carbon cost borne by imported products as closely as possible with that faced by EU domestic producers.

The European Commission has made the following clear:

• In 2026, prices will be published quarterly only;

• Starting in 2027, prices will be published weekly;

• The Q1 2026 price was published on April 7, 2026, at EUR 75.36 per tonne.

The message behind this is clear: CBAM’s pricing mechanism is becoming increasingly normalized and transparent, and companies will find it harder and harder to avoid this cost variable in the future.

Why Should Companies Take This Price Seriously?

From a business operations perspective, EUR 75.36 per tonne is not just a policy figure—it is a key parameter that can directly feed into cost calculations, pricing models, and customer communications.

If a company exports products covered by CBAM, its future compliance cost will ultimately depend on the number of CBAM certificates it must surrender and the applicable CBAM certificate price at the time. Actual compliance outcomes will, of course, also be influenced by factors such as the phased withdrawal of free allowances and rules governing the deductibility of carbon prices already paid in the country of origin. Even so, from a business decision-making standpoint, this price is already sufficient to justify preliminary cost assessment.

How Is CBAM Compliance Calculated?

When many companies see EUR 75.36 per tonne, their first reaction is often: is this price high or low?

In practice, however, two questions matter more:

• the calculation logic behind CBAM compliance costs;

• whether product emissions will ultimately be counted based on actual measured values or default values.

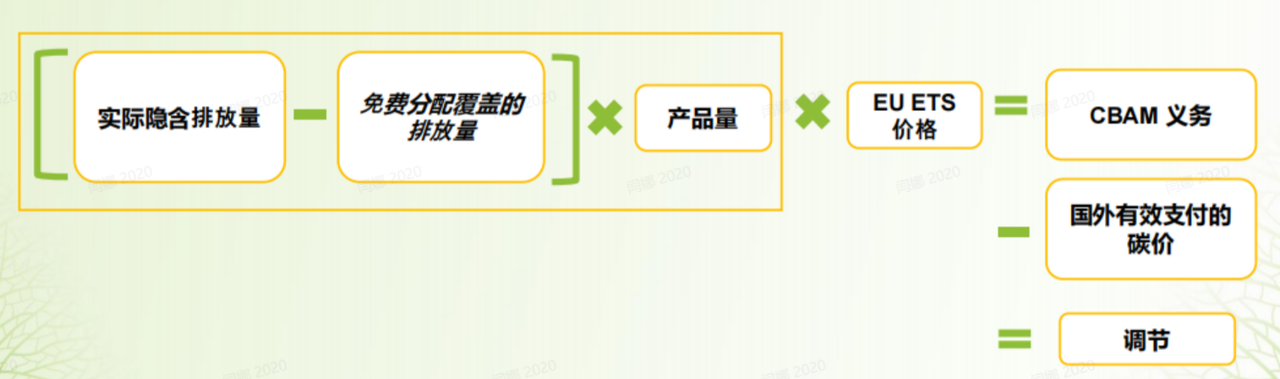

During the formal CBAM phase, a company’s compliance cost must be assessed by combining several factors, including the embedded emissions of the product, the applicable certificate price for the period, the levy ratio corresponding to the phase-out of EU ETS free allowances, and any carbon price already paid in the country of origin that is recognized under the rules.

• First, determine the embedded emissions of the product;

• Then apply the relevant CBAM certificate price for the period;

• At the same time, factor in the CBAM levy ratio linked to the year-by-year phase-out of EU ETS free allowances;

• Finally, deduct any carbon price already paid in the country of origin that is actually paid and recognized under the rules.

(Source: European Commission)

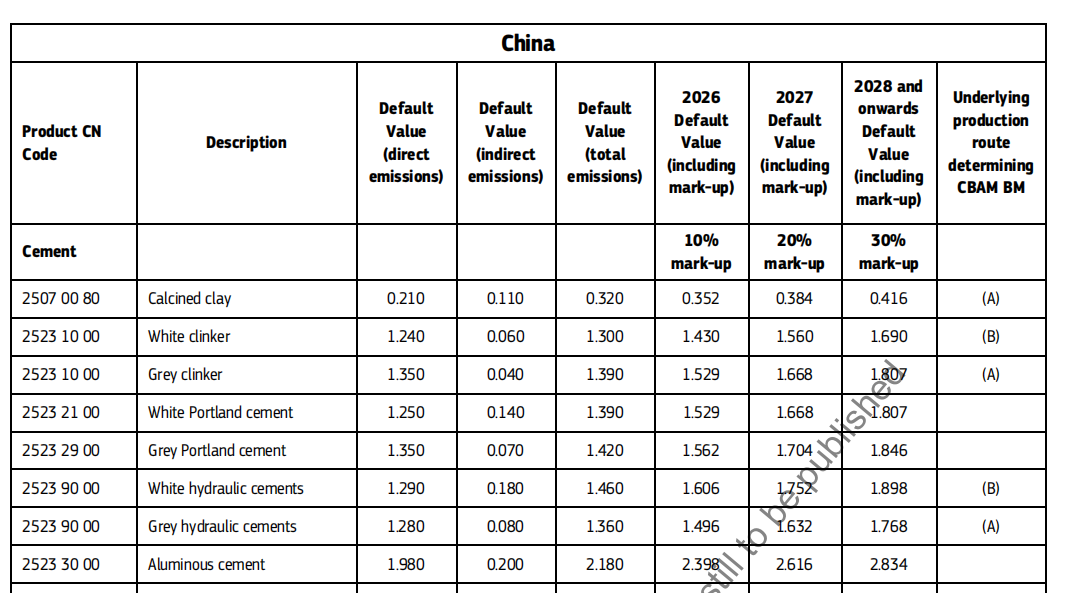

Among all these variables, the one companies can most directly influence through their own data preparation and management capabilities is whether product emissions are calculated using actual measured values or default values. If a company can provide real, complete, compliant, and verified emissions data, it may be able to declare emissions levels that more accurately reflect its actual situation. If it cannot provide usable actual data—or if data boundaries are unclear, the evidence chain is incomplete, or accounting methods are inconsistent—default values may apply, potentially leading to a significant increase in compliance costs. In the steel sector, for example, the default emissions value published under CBAM for semi-finished steel products is 3.169 tCO₂e/t, nearly twice China’s actual level, showing a clear tendency toward distortion. For an import volume of 1,000 tonnes of semi-finished steel, using the default value could increase compliance costs by more than EUR 100,000.

More importantly, these default values are not fixed. They are subject to a year-by-year mark-up mechanism, with the exact method of application subject to formal EU regulations and implementing rules. This means that for exporters, the ability to provide actual measured emissions data is no longer merely a value-add—it is a critical dividing line that will directly affect future compliance costs and customer competitiveness.

(Source: European Commission, Annex to Implementing Act on Default Values)

What Should Exporters Do Now?

At this point in time, companies can begin preparing in at least three directions.

First, establish a reliable emissions data foundation and carbon management system as soon as possible.

Companies should not rely on the idea of “using default values for now.” For products exported to the EU as a priority, businesses should begin mapping process boundaries, energy consumption, and precursor-related data as early as possible, while gradually building clearer carbon data management mechanisms and cross-functional collaboration processes. The earlier a company forms a data foundation based on actual measured values, the better positioned it will be for future reporting, verification, customer communication, and compliance cost control.

Second, closely track policy details and price developments.

In 2026, certificate prices are published quarterly, with Q2, Q3, and Q4 prices still to come. Starting in 2027, prices will be published weekly. As the pricing cycle accelerates, companies will feel carbon cost volatility more directly. At the same time, detailed rules on verification, deductions, and sector coverage also warrant continued attention.

Third, turn “emissions reduction capability” into “market capability.”

Over the longer term, CBAM is not just a compliance burden—it is also pushing companies to optimize their energy mix, improve energy efficiency, adopt green electricity, upgrade processes, and promote low-carbon procurement. Those that can reduce the carbon intensity of their products earlier will be more likely to gain a competitive advantage in the European market.

To respond effectively to CBAM, companies need more than a certificate—they need a carbon data compliance system that can withstand EU verification. Backed by Carbonstop’s self-built global mainstream databases and localized factor libraries, we provide end-to-end CBAM compliance services covering data monitoring, emissions accounting, report generation, and third-party assurance support. We help companies in sectors such as steel, aluminum, and chemicals accurately calculate the embedded emissions of every tonne of product, while also supporting downstream manufacturers in building product carbon footprint governance systems for exports to the EU—helping turn carbon costs into a passport for competing under the new green trade barrier.

Note: The descriptions in this article regarding the CBAM certificate price, release timing, and pricing mechanism are based on public information published by the European Commission’s Directorate-General for Taxation and Customs Union in April 2026. Specific requirements for compliance, accounting, verification, the application of default values, and carbon price deductions remain subject to subsequent formal EU regulations, implementing rules, and guidance from competent authorities.