In 2026, global capital markets have shifted from evaluating corporate sustainability intentions to pricing empirical climate performance. As the Corporate Sustainability Reporting Directive (CSRD) and the International Sustainability Standards Board (ISSB) standards transition into mandatory enforcement, institutional investors face unprecedented pressure to strip greenwashing risks from their portfolios. Fiduciary duty now requires asset managers to treat climate risk through a strictly financial lens.

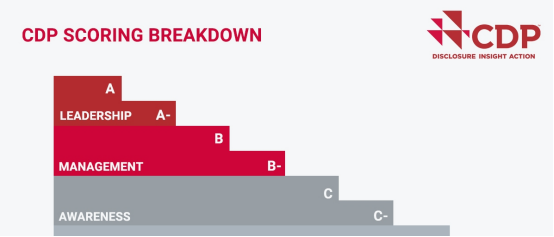

In this hyper-regulated landscape, achieving a Carbon Disclosure Project (CDP) 'A List' rating has evolved from a voluntary environmental milestone into a primary mechanism for capital attraction. For Chief Sustainability Officers (CSOs), the annual CDP disclosure is no longer just a reporting line item; it is a strategic asset that directly influences equity valuations, borrowing costs, and cross-border trade resilience.

The Convergence of Voluntary and Mandatory Frameworks

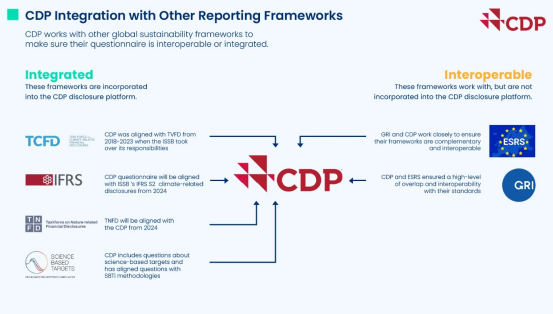

The modern financial ecosystem no longer separates voluntary disclosures from regulatory compliance. Over the past few years, the CDP framework has integrated the quantitative requirements of ISSB (IFRS S2) and CSRD. Consequently, institutional investors utilize a company’s CDP score as an immediate proxy for its global regulatory readiness.

A high CDP score provides structural assurance to global asset managers that an enterprise can withstand upcoming regulatory shocks, such as the accelerating enforcement of the EU Carbon Border Adjustment Mechanism (CBAM).

Furthermore, capital allocation is increasingly tied directly to these verified carbon metrics. Achieving 'A List' status signals to lenders that an organization has mitigated its transition risks, unlocking access to sustainability-linked bonds and green credit lines with highly favorable terms. Conversely, data gaps or a lack of transparency introduce premium risks, leading to systematic divestment and increased borrowing costs as fiduciary constraints tighten globally.

Resolving the Scope 3 Data Granularity Barrier

Moving from a baseline disclosure to the elite 'A List' requires a fundamental shift in data strategy: enterprises must replace broad historical estimates with granular, activity-based tracking. For the average multinational corporation, 80%+ of total carbon exposure resides within Scope 3 emissions, hidden deep within multi-tier supply chains.

Historically, companies relied heavily on spend-based financial averages to calculate these emissions. While acceptable in early reporting cycles, this methodology is no longer sufficient to secure a top-tier CDP rating.

| Data Strategy | Methodology | CDP Scoring Impact | Regulatory & Audit Risk |

| Legacy Approach | Spend-based financial averages | Capped scores; point deductions | High exposure to CBAM audit failures |

| Enterprise Standard | Supplier primary activity data | Maximizes Scope 3 disclosure points | Low; fully audit-ready framework |

To maximize points under the current CDP questionnaire, CSOs must actively engage upstream vendors to collect primary, activity-based data. Carbonstop addresses this operational bottleneck by deploying automated, scalable supplier engagement workflows. This framework lowers the technical barrier for vendors, shifting supply chain data collection from an administrative burden into a continuous, verifiable data stream.

Bridging the Asian Manufacturing Blind Spot

For global corporations operating within or sourcing from Asian manufacturing hubs, the largest obstacle to data integrity is the reliance on generic, Western-centric emission factors. Applying these broad averages to highly localized industrial processes routinely introduces severe calculation errors, inflating a product's carbon footprint or underestimating compliance liabilities.

This regional blind spot is where data precision becomes a competitive advantage. Carbonstop mitigates this risk through the China Carbon Database (CCDB). By integrating extensive, verified, region-specific emission factors into your inventory, the platform eliminates secondary guesswork.

Once captured, this data is processed through the Carbon Cloud (Ccloud) platform, which utilizes AI-driven validation checks to scan massive datasets, flag anomalies, and eliminate calculation errors before submission. This automated digital oversight guarantees absolute data traceability, allowing third-party financial auditors to seamlessly trace emissions data from the corporate balance sheet directly down to individual facility utility bills.

Strategic Execution: Preparing for the Next Cycle

True climate leadership requires embedding carbon management directly into core operational and procurement strategies. By integrating automated carbon accounting software into daily enterprise resource planning (ERP) systems, procurement heads and sustainability managers can establish carbon efficiency as a primary KPI alongside traditional cost and quality metrics.

As you plan your corporate strategy for the upcoming disclosure cycle, passive compliance is no longer sufficient to maintain a competitive market position. CSOs must proactively transform their climate data from a reporting obligation into a clear indicator of market resilience.

Frequently Asked Questions

CDP has fully aligned its annual questionnaire with major global standards, meaning that missing quantitative metrics or vague qualitative descriptions will automatically trigger significant point deductions, making an 'A List' rating impossible without compliance with these standards.

2. Why are spend-based emissions estimates no longer sufficient for securing a top-tier CDP rating?

Spend-based calculations rely heavily on generic financial averages that fail to reflect actual operational efficiencies or real reduction efforts, whereas CDP now heavily rewards companies that utilize primary, activity-based data from their supply chain.

3. What steps can procurement teams take to encourage suppliers to share accurate carbon data?

Procurement leaders should deploy automated supplier engagement platforms that lower the technical barrier for vendors, provide clear educational onboarding, and integrate carbon disclosure metrics directly into preferred supplier selection criteria.

4. How does localized data accuracy impact a global enterprise's vulnerability to carbon regulations like CBAM?

Inaccurate or generalized emission factors can lead to overestimating a product's carbon footprint, resulting in unnecessarily high financial liabilities under border adjustment taxes, or underestimating emissions, which introduces severe compliance and litigation risks.