01 Current Status of the Packaging Industry

With the rapid development of modern commerce and logistics industries, the packaging industry has experienced continuous and stable growth globally.

The proposal of China's dual carbon goals and the widespread adoption of sustainable development concepts have led to improvements in production processes and technology levels across various sectors involving packaging. This has facilitated the gradual trend towards lighter and greener packaging materials.

Low-carbon packaging products and designs are gradually becoming new hotspots in the packaging industry. An increasing number of customers now require their packaging material suppliers to provide relevant product carbon footprint data. More and more packaging companies are beginning to realize that practicing sustainable development concepts requires corporate carbon management and the calculation of the carbon footprint of their products.

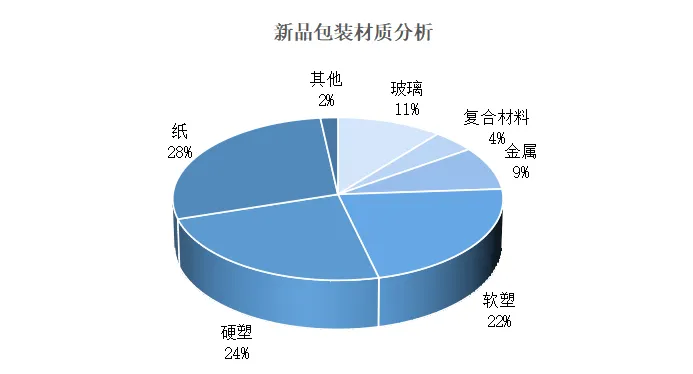

The sources of carbon emissions for packaging industry companies include not only the production equipment used in their own operations but also externally purchased goods, which constitute one of the main sources of emissions under Scope 3. Currently, the primary materials used in the packaging industry include metal packaging, glass packaging, plastic packaging, cigarette cartons, paper packaging, and specialty papers. According to data from the China Packaging Federation in 2021, the specific distribution of new packaging materials is shown in the following chart:

Plastic and paper together account for 74% of new packaging materials. As raw materials, the carbon emissions from the production and processing of plastic and paper in the upstream supply chain of the packaging industry are relatively high. Therefore, many packaging companies are adopting the use of new low-carbon materials and reducing raw material usage as key measures to reduce carbon emissions in their production processes.

......

Becoming a Ccloud paying user allows you to read the full text.